It’s been a wild August for markets.

Recession fears kicked off the worst selloff since 2022 at the beginning of the month.

Then markets staged a choppy recovery, even notching the strongest week of the year along the way. (1)

Market sentiment rollercoaster: Wait a bit, things are bound to change!

That’s not so surprising. It’s very common for a strong recovery to follow a selloff. It’s one of the (many) boring reasons I recommend not abandoning an investing strategy when markets get jittery.

(If you ever feel tempted, please reach out so we can talk.)

I can't predict the future, but I can show you what has historically happened and offer reassurance.

So, what could happen next for markets?

I expect more volatility ahead, but that’s really not a grand prediction. Markets are usually volatile! Despite renewed recession fears, fresh data seems to have eased investor anxiety and boosted hopes that a recession-free “soft landing” is still achievable. That's good news for markets, but there are plenty of risks to watch.

Let’s take a look.

What positive factors could push markets higher?

Inflation continues to head downward, which is good news for consumers and supports the case for interest rate cuts this year. (2)

Other economic data is also showing optimism. Retail sales jumped unexpectedly, suggesting American consumers are doing better than expected. (3) Since consumer spending accounts for about 70% of U.S. economic growth, it’s a big indicator of economic health.

Analysts currently expect the Federal Reserve to cut interest rates in September. (4) Notes from the last Federal Open Market Committee meeting showed that policymakers are close to cutting rates, supporting hopes for a September cut. (5)

What negative factors could trigger a selloff?

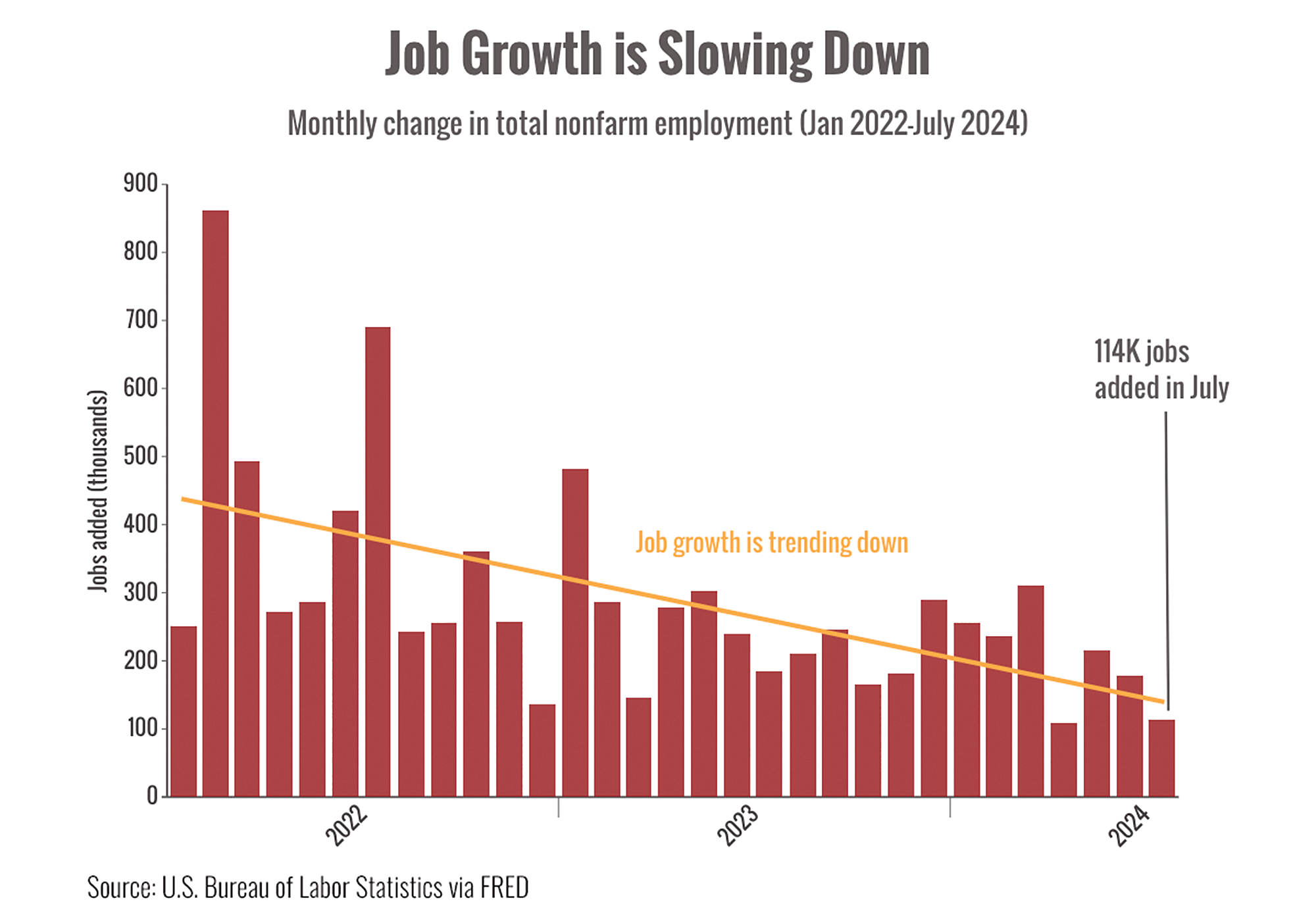

The labor market is showing cracks. The unemployment rate ticked up in July to its highest level since October 2021, and job growth slowed more than expected. (6)

You can see in the chart above that job creation has been slowing down over the past two years. That's not entirely surprising since the labor market has been recovering from pandemic disruptions.

However, a recently released annual revision of job data showed that the economy added nearly 30% fewer jobs over the last 12 months than originally reported. (7) If the labor market weakens and Americans start to worry about their financial situation, it could erode consumer confidence and spending later in the year.

The past few weeks have shown us how easy it is for investors to lose their optimism in a selloff…

And then quickly regain it in a recovery. While markets tend to reflect the economy in the medium and long term, the opposing emotions of fear and greed tend to have greater influence in the short term. We’re seeing a lot of reasons to be optimistic, but we're also watching some clouds on the horizon.

Though it doesn’t seem likely that a recession is here or even around the corner, we’re monitoring the data closely.

And how about market technicals?

As a student of market technical behavior, there are plenty of positives that don't seem to get much attention. Given the news headlines right now, I'd say they're even more noteworthy. (Bonus points for bringing one or more of these up at your next cocktail party!)

Similar to the broad US stock market, most developed countries outside the US are above their respective 200-day moving averages, a common benchmark to determine whether markets are generally rising or falling. Even some emerging market countries like Taiwan, Malaysia and India pass this trend test.

The number of New York Stock Exchange (NYSE) advancing stocks minus declining stocks is at new highs. For now, this shows solid "breadth" behind the move higher in major indexes.

This should be intuitive: In order for markets to move lower, we would need to see an increasing number of individual stocks moving lower. Despite August's volatility, we've seen no significant increase in the number of stocks hitting new monthly, quarterly or yearly lows. Quite the opposite: In July we saw the largest number of NYSE stocks hitting yearly highs since the post-Covid bounce in spring 2021. This suggests increasing⏤not waning⏤participation.

Finally, remember the S&P 500 is a market capitalization weighted index. This means the largest stocks like Apple, Microsoft and Nvidia have the biggest weightings and are a combined nearly 20% of the index. While this index has been strong, even its equal-weighted version (where the largest stock is only about 0.25% of the index) is also at new highs. As a result, this index has larger weights in the Financial, Industrial and Healthcare sectors. Some view this as broader market participation vs. just a handful of technology stocks.

As always, things can change quickly, so stay tuned!

∞

Sources:

1. https://www.cnbc.com/2024/08/18/stock-market-today-live-updates.html

2. https://www.bls.gov/news.release/cpi.nr0.htm

3. https://www.cnbc.com/2024/08/15/retail-sales-july-2024-.html

4. https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

5. https://www.cnbc.com/2024/08/21/fed-minutes-july-2024.html

Chart source: https://fred.stlouisfed.org/series/PAYEMS#0, trend line is linear